Global Market Weekly Recap: September 11 – 15, 2023

[ad_1] Risk assets were generally on top this week thanks to net positive economic updates from the U.S. and stimulative efforts from China, supporting “soft landing” bets. Meanwhile, European currencies like EUR, GBP, and CHF lost pips as disappointing data releases highlighted the growth concerns in the region. So, how exactly did the major global

[ad_1]

Risk assets were generally on top this week thanks to net positive economic updates from the U.S. and stimulative efforts from China, supporting “soft landing” bets.

Meanwhile, European currencies like EUR, GBP, and CHF lost pips as disappointing data releases highlighted the growth concerns in the region.

So, how exactly did the major global assets behave this week? I can explain, but lemme show you the biggest headlines first:

Notable News & Economic Updates:

🟢 Broad Market Risk-on Arguments

The PBoC set the USD/CNY reference rate at 7.3437 vs. market projected rate of 7.2148. The record-high gap underscored the central bank’s aggressiveness in defending the yuan’s strength.

BOE policymaker Catherine Mann said on Monday she’d likely support further rate hikes to fight inflation

Overseas visitor arrivals into New Zealand continued to rebound a year on from fully opening the border, with short-term visitors up from 11.3% to 19.8% in July

Germany ZEW Economic Sentiment: -11.4 (-14.0 forecast; -12.3 previous)

Chinese property developer giant Country Garden secured approval from its creditors to extend repayments on six onshore bonds by three years

U.S. CPI for August: 0.6% m/m (0.5% m/m forecast; 0.2% m/m previous); Core CPI: 0.3% m/m (0.2% m/m forecast/previous)

U.S. Retail Sales in August: 0.6% m/m (0.4% m/m forecast; 0.5% m/m previous)

U.S. Producer Prices Index for August: 0.7% m/m (0.4% m/m forecast/previous); core PPI at 0.2% m/m as expected (0.4% m/m previous)

On Thursday, The People’s Bank of China announced another cut the reserve requirements for cash lenders by 25 bps to 7.4%

Chinese industrial production accelerated from 3.7% y/y to 4.5% in August vs. an estimated increase to 3.9%

Chinese retail sales rose from 2.5% y/y to 4.6% in Aug vs. projected improvement to 3.0%

🔴 Broad Market Risk-off Arguments

Over the weekend, BOJ Gov. Ueda gave an interview with Yomiuri and implied that the central bank may have enough information about wage hikes by the end of 2023 to possibly reevaluate its monetary policies.

Japan’s machine tool orders dipped by 6.3% m/m in July (-19.7% y/y) and marked its first monthly decline in two months.

U.K.’s GDP surprisingly contracted by 0.5% m/m in July (vs. -0.2% expected, 0.5% previous) after strikes in hospitals and schools as well as unusually rainy weather weighed on output

U.K.’s unemployment rate higher from 4.2% to 4.3% in August; Jobless claimants are lower from 29K to 0.9K; Average wage growth still at 8.5% record high in July; net jobs change was -207K, far below -80K forecast

Australia’s unemployment rate remained at 3.7% in August; Participation rate edged up from 66.9% to 67.0%; Employment gains higher at 64.9K (vs. 25.4K expected, -1.4K previous) but part-time gains (+62.1K) outpaced full-time job increases (+2.8K)

The European Central Bank raised the deposit rate from 3.75% to 4.00% on Thursday; Lagarde does not signal that this may be the peak

University of Michigan U.S. Consumer Sentiment, preliminary September read at 67.7 vs. 69.5 in August

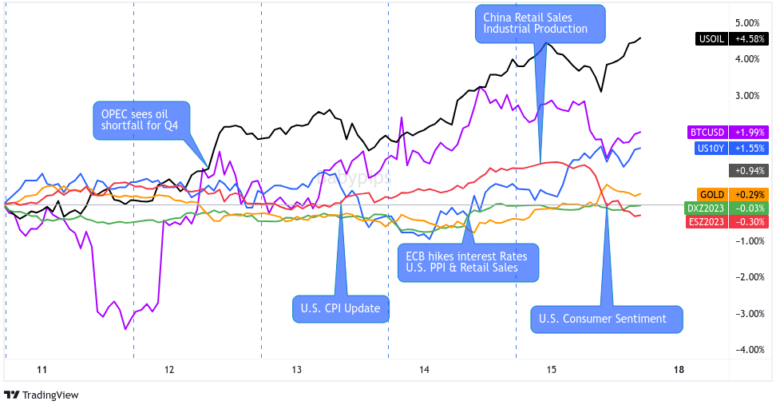

Global Market Weekly Recap

Dollar, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

It was the Japanese yen that started the trading week with a bang. Weekend comments from Bank of Japan (BOJ) Governor Kazuo Ueda suggested that the central bank may exit its negative interest rate era as early as January next year. I guess they’re just “quiet quitting” these days, huh?

Japan’s 10-year government bond yields rose to their highest levels since 2014 and the Japanese yen jumped by about 1% to hit its strongest levels in a week against the U.S. dollar.

AUD and NZD bulls were also energized on Monday, this time thanks to the People’s Bank of China (PBOC) not-so-subtly reminding the markets that they should “resolutely avoid behaviors that disturb market orders such as conducting speculative trades.” TL;DR: Don’t short the yuan.

JPY, AUD, and NZD’s gains, coupled with bets that this week’s U.S. data releases would support less hawkish Fed policies, weighed on the U.S. dollar and supported assets such as gold and equities.

Tuesday’s price action was a bit more mixed as traders waited for Wednesday’s U.S. CPI release. In fact, we didn’t see much volatility until the start of the London session when the U.K. printed its August jobs numbers.

While the U.K. saw a higher unemployment rate and lower participation rate, we also saw lower initial jobless claimants and more full-time workers. More importantly, wage growth remained sticky at 8.5% in the three months to July and supported further tightening for the Bank of England (BOE).

Growth watchers who were sweating bullets at the already high U.K. interest rates didn’t like the hawkish update. GBP spiked lower at the news and saw minimal pullback by the end of the day.

Crude oil was also under the spotlight as WTI crude oil prices hit fresh 10-month highs. And why not? OPEC shared that we’ll likely see the biggest global oil inventories deficit since 2007 as early as Q4 2023. Ditto for the U.S. Energy Information Administration (EIA), which predicted that consumption would outstrip production by 230,000 barrels a day in Q4 2023.

It was a bad day to be knowledgeable about supply and demand but a good day for oil bulls. USOIL started the day near $87.00 but closed near the $89.30 levels. Yipes!

Higher oil price concerns and profit-taking ahead of the U.S. CPI report weighed on U.S. equities. AAPL shares even got an extra push lower when its iPhone 15 launch inspired a buy-the-rumor, sell-your-kidney type of price action.

Wednesday wasn’t much better in terms of market direction. GBP spiked lower at the U.K.’s surprisingly weak monthly GDP report but the moves were quickly reversed before the U.S. session started.

Even the anticipated U.S. CPI event was (mostly) a dud. Both the U.S. headline and core CPI exceeded market expectations, but not wildly enough to convince the markets that the Fed would raise its interest rates next week.

U.S. 10-year government bond yields spiked to 4.35% before plunging to new weekly lows closer to 4.24% while the U.S. equities ended the day in the green.

The winners and losers were clearer on Thursday as growth concerns set in. AUD and NZD, for example, erased all of their initial gains when an Australian jobs report showed stronger-than-expected job creation but also lower average hours and more part-time job creation than full-time workers.

As expected, the European Central Bank (ECB) also raised its interest rates by 25 basis points to 4.50%. But ECB President Lagarde also hinted that (a) the central bank has hit “peak rates” and that (b) they’ll keep their interest rates high for a long time period.

The markets gave a side eye on the “higher for longer” bit and worried about what it would mean for the region’s growth. EUR dropped across the board and took fellow European currencies like GBP and CHF along with it.

Meanwhile, stronger-than-expected retail sales and PPI reports in the U.S. supported “soft landing” bets and pushed non-European risk assets higher.

USOIL resumed its uptrend to new intraweek highs near $90.60; Bitcoin (BTC/USD) saw a slow and steady climb to $26,800; CAD saw support from higher oil prices, and U.S. equity indices closed in the green. Meanwhile, U.S. 10-year yields touched new weekly lows near 4.22% and the non-yielding gold hit new weekly lows just above $1,900.

Market volatility cooled on Friday through the Asia and London sessions, picking up mostly in equities, oil and crypto in the early U.S. session. This was soon followed by a pop in gold prices, signaling a shift back to risk aversion flows.

There doesn’t seem to be a singular catalyst for the behavior, so it’s possible traders were digesting different headlines & data that made arguments against the “soft landing” and peak inflation narratives.

The most notable contributors were likely the higher U.S. import & export prices update, a publicly huge wage battle between union workers and automotive workers in the U.S., and weaker-than-expected U.S consumer sentiment reads.

[ad_2]

لینک منبع : هوشمند نیوز

آموزش مجازی مدیریت عالی حرفه ای کسب و کار Post DBA آموزش مجازی مدیریت عالی حرفه ای کسب و کار Post DBA+ مدرک معتبر قابل ترجمه رسمی با مهر دادگستری و وزارت امور خارجه |  آموزش مجازی مدیریت عالی و حرفه ای کسب و کار DBA آموزش مجازی مدیریت عالی و حرفه ای کسب و کار DBA+ مدرک معتبر قابل ترجمه رسمی با مهر دادگستری و وزارت امور خارجه |  آموزش مجازی مدیریت کسب و کار MBA آموزش مجازی مدیریت کسب و کار MBA+ مدرک معتبر قابل ترجمه رسمی با مهر دادگستری و وزارت امور خارجه |

مدیریت حرفه ای کافی شاپ |  حقوقدان خبره |  سرآشپز حرفه ای |

آموزش مجازی تعمیرات موبایل آموزش مجازی تعمیرات موبایل |  آموزش مجازی ICDL مهارت های رایانه کار درجه یک و دو |  آموزش مجازی کارشناس معاملات املاک_ مشاور املاک آموزش مجازی کارشناس معاملات املاک_ مشاور املاک |

- نظرات ارسال شده توسط شما، پس از تایید توسط مدیران سایت منتشر خواهد شد.

- نظراتی که حاوی تهمت یا افترا باشد منتشر نخواهد شد.

- نظراتی که به غیر از زبان فارسی یا غیر مرتبط با خبر باشد منتشر نخواهد شد.

ارسال نظر شما

مجموع نظرات : 0 در انتظار بررسی : 0 انتشار یافته : 0