Global Market Weekly Recap: October 2 – 6, 2023

[ad_1] October is here, and you know what that means: another round of top tier events to start the month, including the monthly monster U.S. employment update! Traders patiently awaited the event before making big moves, patience that was rewarded with a big positive surprise and volatility to follow! Not caught up on the major

[ad_1]

October is here, and you know what that means: another round of top tier events to start the month, including the monthly monster U.S. employment update!

Traders patiently awaited the event before making big moves, patience that was rewarded with a big positive surprise and volatility to follow!

Not caught up on the major headlines? Check’em out before seeing how it all played out!

Notable News & Economic Updates:

🟢 Broad Market Risk-on Arguments

China’s official manufacturing PMI improved from 49.7 to 50.2 in September; non-manufacturing PMI higher from 51.0 to 51.7

Congress passed bill to keep the government open, averting a shutdown for at least 45 days

ISM U.S. Manufacturing PMI for September: 49.0 (48.1 forecast; 47.6 previous); Prices Index decreased to 43.8 (48.9 forecast; 47.9); Employment Index increased to 51.2 vs. 48.5 previous

Eurozone’s HCOB services PMI adjusted slightly higher from 48.4 to 48.7 in September

U.K. shop price inflation eased from 6.9% to 6.2% in September, its lowest in a year – BRC

Switzerland’s consumer prices decreased by 0.1% in September (vs. 0.0% expected, 0.2% previous)

Canada Employment Change for September: +63.8K (10K forecast; 39.9K previous); Unemployment Rate stayed at 5.5% vs. 5.6% forecast

U.S Non-Farm Payrolls Change in September: 336K (150K forecast; August revised up to 227K from 187K); Average hourly earnings came in below expectations at 0.2% (0.3% forecast)

J.P.Morgan Global composite PMI for September: 50.5 vs. 50.6 in August

🔴 Broad Market Risk-off Arguments

HCOB Germany Manufacturing PMI for September: 39.6 vs. 39.1 in August; factory employment fell for 3rd month in a row; input and purchasing prices continue to fall

European Central Bank Chief Economist Philip Lane commented on Tuesday that more work is still needed as inflation rate is still well above 2%

S&P Global / CIPS UK Manufacturing PMI for September: 44.3 vs. 43.0 previous

Japan’s au Jibun Bank manufacturing PMI revised lower from 48.6 to 48.5; “Manufacturing conditions deteriorate at sharper rate in September”

As expected, the RBNZ kept its interest rates steady at 5.50% in October, but with a less hawkish-than-expected statement

As expected, the RBA kept its interest rates at 4.10%; “Some further tightening of monetary policy may be required”

Canada Average Hourly Earnings rose by 4.2% y/y (4.1% y/y forecast; 4.3% y/y previous)

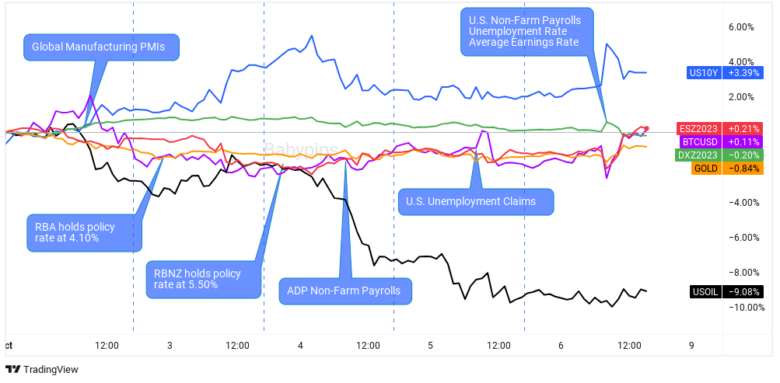

Global Market Weekly Recap

Dollar, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

The calendar flipped to October this week, and as usual with the start of every new month, the forex calendar hit traders with a slew of top tier economic events to watch.

The most notable events included the final global business sentiment survey reads for September, monetary policy statements from the Reserve Bank of Australia and Reserve Bank of New Zealand, and the highly anticipated U.S. government’s employment situation report on Friday.

This can often elevate volatility and create short-term opportunities, but price and volatility this week was mostly choppy and subdued relative to recent weeks. Instead, we saw a steady continuation of U.S. dollar strength and rising bond yields. This is likely due to traders continuing to price in the “higher for longer” interest rate theme as inflation data continues to point to interest rates remaining well above target levels.

The bond yield environment likely put pressure on the other major financial asset classes, on the idea that higher interest rates will continue to slow economic growth, but also on the idea that U.S. bonds are growing to be a better risk adjusted investment as yields move higher, at least for those who aren’t in the bond markets yet.

For those who have been holding bonds for a while, though, the bond market has been a big pain, characterized by another fall in Treasury bond futures, falling ~ -2.50% to start the new month.

Going back to the data, the final reads for September global PMI signaled less net negative conditions, with many also signaling easing inflation rates. Unfortunately, we’re also seeing continued negative sentiment in the employment sector in many countries as new orders and demand fall, especially in the European region.

The U.S. remained an outlier once again as U.S. businesses saw net expansionary conditions in the services sector, while the negative sentiment in the manufacturing sector improved and almost made its way back to expansionary territory.

As far as monetary policy, both the RBNZ and RBA held their main policy rates as-is (5.50% and 4.10% respectively). This was as expected, but unexpectedly the tone did shift a little less hawkish in both of their statements, citing slowing economic conditions. But both central banks also kept the door open to further hikes if inflation conditions warranted such moves in the future.

As for U.S. jobs data, as always we got a steady stream of updates, and it was a bit of a rollercoaster leading up to the main report on Friday.

The ISM Manufacturing Employment Index and JOLTS job openings were net positive and lifted jobs sentiment to start the week, which was then pulled back after the much lower-than-expected ADP private payrolls report and a slightly less optimistic ISM Services Employment Index read on Wednesday.

On Thursday, the weekly U.S. initial jobless claims data came in below expectations at 207K, which was an appropriate read leading up a very strong Non-Farm Payrolls change number on Friday. The U.S. saw a net addition of 336K jobs in September, and revised the August number higher to 227K from 187K.

This sparked pretty big moves across the broad markets, unsurprisingly a spike higher in the U.S. dollar and bond yields. This was a short-lived move, though, as traders began to price in the lower-than-expected average earnings number at 0.2% (0.3% forecast) and the tick higher in the unemployment rate from 3.7% to 3.8%. These reads supported slowing inflation and economic growth expectations narratives.

All markets reversed on that sentiment, potentially on raised odds of the “soft landing” scenario (i.e., inflation rates gets back to target with little to no recessionary conditions). Some markets even surpassed pre-event levels on the reversal, but unfortunately for any bull in most of the major markets outside of the U.S. dollar, this didn’t appear to be enough to get back in the green ahead of the Friday close.

Given all that happened, most markets aren’t too far from the week open, with two exceptions: oil prices and the Japanese yen.

On Tuesday, USD/JPY hit the closely watched 150.00 level, which many traders speculated as the line in sand where the Japanese officials would intervene in the Japanese yen. After spending about 10 minutes above 150.00, the spiked higher against all major currencies, with USD/JPY bottoming out around 147.30 five minutes later and whipping back to the 149.00 handle, where it’s been since. The Bank of Japan has remained silent on the event, but early evidence suggests that it was not likely due to Japanese intervention.

The yen move was crazy but the most notable move of the week goes to the big change in oil prices as it shed over -13% from its recent swing highs around the $95/barrel handle.

This was likely due to some mix of factors including falling business sentiment survey data, a strong U.S. dollar and possibly speculation that no further deep production cuts may be ahead from OPEC.

Whatever the case may be, WTI crude oil is now trading just below the $83 handle, giving back all of its September gains and now below the August swing high of just under the $85 handle.

[ad_2]

لینک منبع : هوشمند نیوز

آموزش مجازی مدیریت عالی حرفه ای کسب و کار Post DBA آموزش مجازی مدیریت عالی حرفه ای کسب و کار Post DBA+ مدرک معتبر قابل ترجمه رسمی با مهر دادگستری و وزارت امور خارجه |  آموزش مجازی مدیریت عالی و حرفه ای کسب و کار DBA آموزش مجازی مدیریت عالی و حرفه ای کسب و کار DBA+ مدرک معتبر قابل ترجمه رسمی با مهر دادگستری و وزارت امور خارجه |  آموزش مجازی مدیریت کسب و کار MBA آموزش مجازی مدیریت کسب و کار MBA+ مدرک معتبر قابل ترجمه رسمی با مهر دادگستری و وزارت امور خارجه |

مدیریت حرفه ای کافی شاپ |  حقوقدان خبره |  سرآشپز حرفه ای |

آموزش مجازی تعمیرات موبایل آموزش مجازی تعمیرات موبایل |  آموزش مجازی ICDL مهارت های رایانه کار درجه یک و دو |  آموزش مجازی کارشناس معاملات املاک_ مشاور املاک آموزش مجازی کارشناس معاملات املاک_ مشاور املاک |

- نظرات ارسال شده توسط شما، پس از تایید توسط مدیران سایت منتشر خواهد شد.

- نظراتی که حاوی تهمت یا افترا باشد منتشر نخواهد شد.

- نظراتی که به غیر از زبان فارسی یا غیر مرتبط با خبر باشد منتشر نخواهد شد.

ارسال نظر شما

مجموع نظرات : 0 در انتظار بررسی : 0 انتشار یافته : 0