FX Weekly Recap: September 18 – 22, 2023

[ad_1] The week’s primary focus revolved around central bank actions in response to persistent inflation and economic slowdown signals. The New Zealand dollar emerged as the top-performing currency, while the British pound struggled to last place as sentiment stemming from the Bank of England’s recent shift in policy stance weight on Sterling. Missed the major

[ad_1]

The week’s primary focus revolved around central bank actions in response to persistent inflation and economic slowdown signals.

The New Zealand dollar emerged as the top-performing currency, while the British pound struggled to last place as sentiment stemming from the Bank of England’s recent shift in policy stance weight on Sterling.

Missed the major forex headlines? Here’s what you need to know from last week’s FX action:

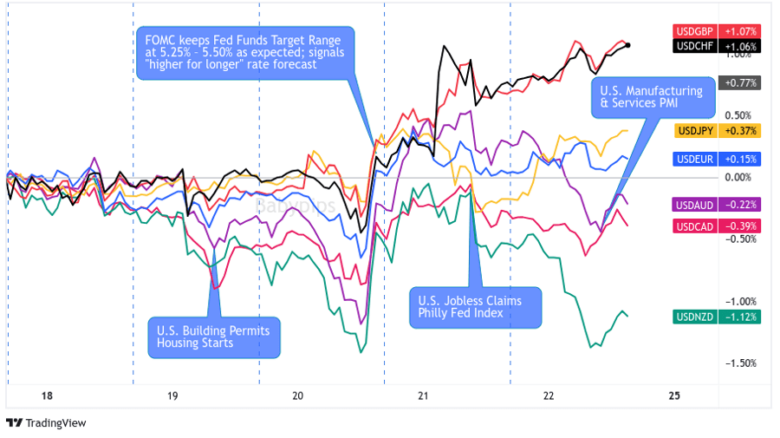

USD Pairs

Overlay of USD vs. Major Currencies Chart by TradingView

The U.S. dollar was driven once again by Fed speculation, but this time we got speculation confirmation with the FOMC giving us their latest monetary policy statement.

They made no changes to the Fed funds target range as expected, but what was unexpected by many was the hawkish lean taken by the committee, essentially signaling a high probability of another hike in 2023 and a low probability of significant cuts in 2024.

This brought the Dollar back from a big pre-event dip, but it wasn’t enough to keep the Greenback in the green as another positive U.S. weekly initial jobless claims update on Thursday seems to have sparked some risk-on vibes to mix up USD’s performance at the end of the week.

🟢 Bullish Headline Arguments

U.S. Preliminary Building Permits for August: 1.54M (1.43M forecast; 1.44M previous)

On Wednesday, the Fed kept its Fed funds target range at 5.25% – 5.50% as expected; The Fed’s dot plot forecasts pointed to at least one more rate hike in 2023 and “only” a 50bps rate cut in 2024 (from a 100bps rate cut estimated in June)

U.S. initial jobless claims dropped by 20K to an eight-month low of 201K

U.S. current account deficit unexpectedly narrowed from $214B to $212B in Q2 and reflected surpluses on services and primary income that were mostly offset by higher goods deficit

🔴 Bearish Headline Arguments

NAHB U.S. housing index down from 50 to 45 in September; “High mortgage rates are clearly taking a toll on builder confidence and consumer demand”

U.S. Existing Home Sales for August: -0.7% m/m to 4.04M units (1.5% m/m forecast; -2.2% m/m previous)

Philadelphia Fed Manufacturing activity index contracted, down from 12.0 to -13.5 in September

U.S. Flash Manufacturing PMI for September: 48.9 vs. 47.9; greater hiring activity but sales & demand environment remains muted

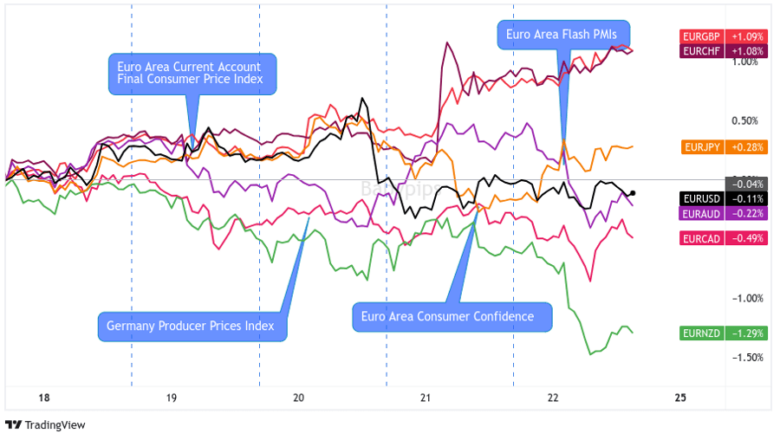

EUR Pairs

Overlay of EUR vs. Major Currencies Chart by TradingView

Throughout the week, the Euro displayed a mixed performance, suggesting that the influence of counter currencies was more pronounced than the impact of European news and data releases.

However, on Friday, there was a uniform bearish trend in the Euro’s price as disappointing updates were released regarding the Euro area Purchasing Manager’s Survey data. This negative data seemed to overshadow any positive factors, contributing to a downward pressure on the Euro’s value.

In the broader context, the Euro ended the week as a net loser against most major currencies, except for the Swiss franc and the British pound, both of which faced bearish pressure themselves after their respective central banks unexpectedly decided to hold off on rate hikes.

🟢 Bullish Headline Arguments

In an interview late Thursday, ECB Chief Economist Philip Lane said interest rates have reached a level that could help bring down inflation but that the ECB will set them “at sufficiently restrictive levels for as long as necessary.”

🔴 Bearish Headline Arguments

Eurozone’s current account surplus shrank from 35.8B EUR to 20.9B EUR in July

Eurozone’s final headline CPI was adjusted from 5.3% to 5.2% y/y; core CPI steady at 5.3% y/y

Germany’s producer prices gained by 0.3% (-12.6% y/y) in August and marked the fastest annual decline since the records started in 1949

Euro Area Flash Consumer Confidence Index for September: -17.8 (-17.3 forecast; -16.0 previous)

HCOB Flash Eurozone PMI for September: 43.4 vs. 43.5 in August; falling confidence in year-ahead outlook as new orders fall; input prices rose at a much faster pace than output prices

HCOB Flash Germany PMI for September: 39.8 vs. 39.1 previous; demand for goods and services continued to drop; output prices rose at the slowest rate since Feb. 2021; employment fell in Q3 as companies remain cautious

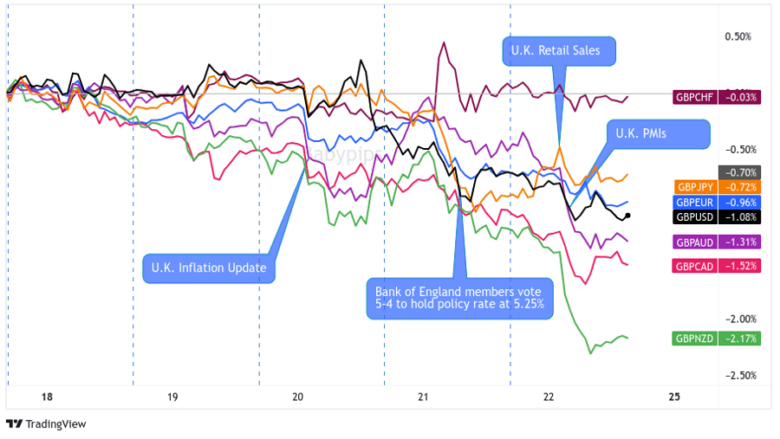

GBP Pairs

Overlay of GBP vs. Major Currencies Chart by TradingView

The British Pound had a bit of a rough week, to be honest. It was on a downward slide most of the time, and that was mainly because of previous comments from the Bank of England that they didn’t need to raise interest rates anymore. This cautious attitude from the central bank seemed to worry investors, and it put a damper on the Pound’s value.

Two events really put the Pound in the hot seat. First, there were those U.K. inflation numbers on Wednesday – they didn’t look too great and probably made folks nervous about the economy.

Then, on Thursday, the Bank of England made a close call with a 5-4 vote to keep interest rates steady at 5.25%. That decision, even though it wasn’t unanimous, sent a mixed message and added to the Pound’s troubles.

🟢 Bullish Headline Arguments

GfK: U.K.’s consumer confidence rose from -25 to -21 (vs -26 expected), its highest level since January 2022

U.K.’s retail sales rebounded by 0.4% in August (0.5% expected, -1.1% previous) on a rebound after a month of wet weather

🔴 Bearish Headline Arguments

Rightmove: “More than a third of U.K. properties have had at least one price reduction, the highest figure recorded since January 2011…Average size of the price reduction is also the highest since January 2011”

U.K.’s inflation surprisingly weakened in August, with the annual headline CPI rising by 6.7% (vs. 7.0% expected, 6.8% previous) and core CPI gaining by 6.2% (vs. 6.8% expected, 6.9% previous) led by decelerations in food prices

U.K.’s producer input prices fell by 2.3% ytd/y in August (vs. -3.2% in July) while output/factory gate prices dipped by 0.4% ytd/y (vs. -0.7% in July)

The Bank of England held their main policy rate at 5.25% on Thursday, largely expected after a lower-than-expected U.K. CPI read earlier, with a vote of 5-4 for holding.

U.K. Public Net Borrowing (ex PSNB) for August was £11.6B, £3.5B more than in August 2022, the 4th highest level of any August on record but less than the OBR forecast of £11.6B

U.K. Flash Manufacturing PMI for September: 44.2 vs. 43.0 previous; Services PMI at 47.2 vs. 49.5

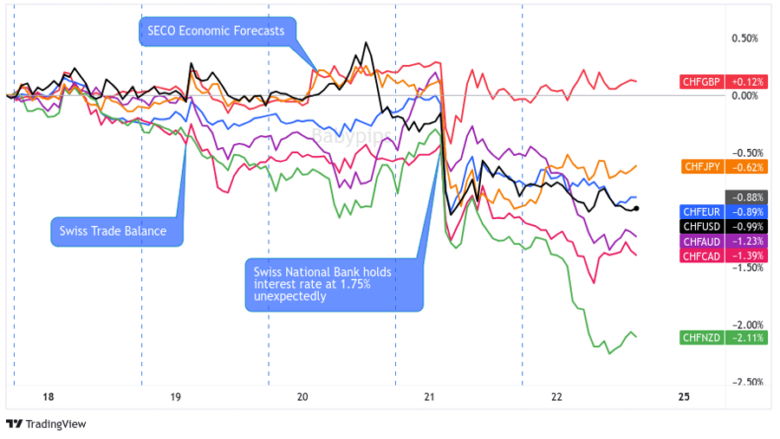

CHF Pairs

Overlay of CHF vs. Major Currencies Chart by TradingView

The Swiss Franc had a bit of a downer week, no sugarcoating it. Things took a sour turn when the Swiss National Bank (SNB) decided to keep their key interest rate at 1.75%, contrary to what many folks were expecting – a 25 basis points hike.

It was like the SNB pulled a surprise move, and it left a mark on the Swiss Franc’s value. To be fair, some recent data had hinted that the SNB might hold off on hiking rates, but it still caught a lot of folks off guard, leading to some bearish vibes in the Franc’s price all the way to the weekend.

🟢 Bullish Headline Arguments

Switzerland’s trade surplus widened from 3.13B CHF to 4.05B CHF in August as exports (+5.9% m/m) outpaced imports (+1.5% m/m)

SECO Swiss Economic forecast for 2023 was upgraded to 1.3% vs. 1.1% previous; 2024 forecast was lowered from 1.5% to 1.2%

🔴 Bearish Headline Arguments

The Swiss National Bank held their main policy rate at 1.75% on Thursday, slightly unexpected, and kept the door open for more action if needed

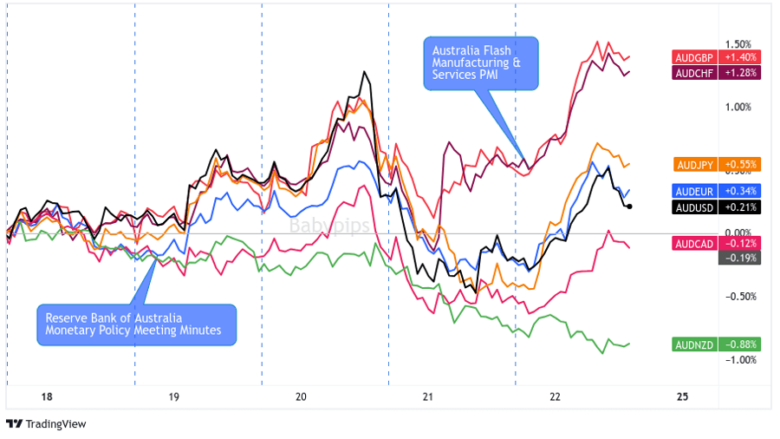

AUD Pairs

Overlay of AUD vs. Major Currencies Chart by TradingView

The Aussie dollar was one of the top performers this week, and without a whole lot of positive updates, it’s likely continued positive sentiment sparked earlier by the recent boost in stimulative efforts from China.

But there were a few bumps in the road. When the Fed threw some hawkish vibes into the mix, Aussie traders didn’t like it one bit. However, it did a bit of a bounce-back dance on Friday. That happened right around the time Australia’s Composite PMI (Purchasing Managers’ Index) shot up, indicating that business sentiment in the land Down Under was climbing back into the green territory.

So, in a nutshell, the Australian Dollar had a rollercoaster week, but it managed to ride the ups and downs, showing that it’s got some resilience in its pocket.

🟢 Bullish Headline Arguments

Australia services PMI picked up from 47.8 to a four-month high of 50.5

🔴 Bearish Headline Arguments

RBA minutes: Members considered a rate hike but chose to hold over risks that the economy could slow more than forecast

Westpac-Melbourne Institute Leading Index slightly improved from -0.56% in July to -0.50% in August; negative prints suggest that “the economy is likely to grow at a below-trend pace”

Judo Bank flash Australian PMIs showed manufacturing PMI down from 49.6 to a three-month low of 48.2;

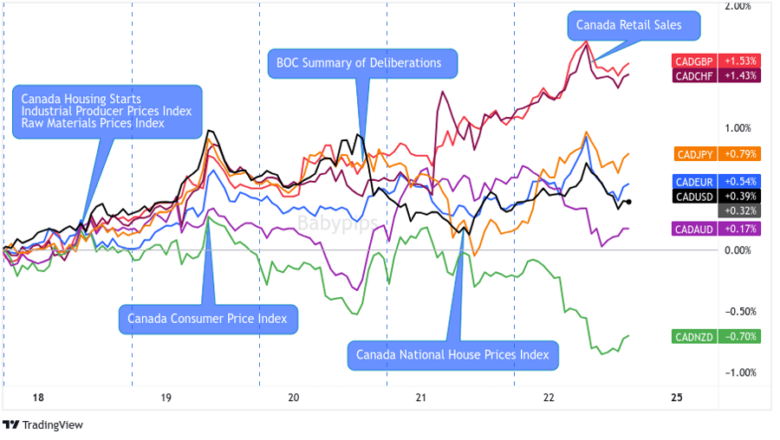

CAD Pairs

Overlay of CAD vs. Major Currencies Chart by TradingView

The Canadian Dollar kicked off the week like a champ, showing off its muscles against major currencies and only giving in to the Kiwi dollar by the time Friday rolled around. We did see a dip on Tuesday after a higher than expected inflation update from Canada, possibly from profit taking and/or a turn in focus towards falling oil prices.

Risk sentiment dominated on Wednesday as the whole world reacted to a hawkish Fed statement, prompting some losses for the Loonie against the majors (except the Aussie and Kiwi), but it wasn’t too long for the bulls to regain their control, likely with the help from rising oil prices after news hit the wires that Russia will temporarily banned fuel exports to support their local fuel economy.

🟢 Bullish Headline Arguments

Canada Housing Starts for August: 244K vs. 242K in July – CMHC

Canada Raw Material Prices Index for August: 3.0% m/m (2.7% m/m forecast; 3.5% m/m previous); Industrial Producer Prices Index: 1.3% m/m (0.5% m/m; forecast; -0.1% m/m previous)

Canada CPI for August: 4.0% y/y (3.9% y/y forecast; 3.3% y/y previous); Core CPI at 3.3% y/y (3.5% y/y forecast; 3.2% y/y previous)

Canada New Housing Price Index for August: 0.1% m/m (-0.3% m/m forecast; -0.1% m/m previous)

Canada Retail Sales for July: 0.3% m/m to C$66.1B (0.2% m/m forecast; 0.1% m/m previous); Core retail sales was up 1.3% m/m

Summary of Governing Council Deliberations: Council still sees a possibility where monetary policy was not yet restrictive enough

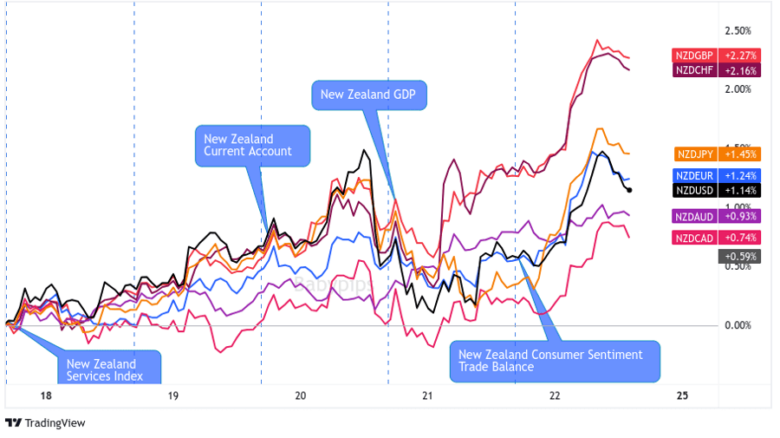

NZD Pairs

Overlay of NZD vs. Major Currencies Chart by TradingView

Well, well, well, the New Zealand Dollar had itself a pretty good week, possibly on the good vibes coming from the Asia region, especially after China flexing its economic stimulus muscles lately.

And even though the economic data updates were like a mixed bag of tricks, there were some bright spots. The big winner was the GDP surprise – it came in higher than everyone thought.

And that’s always a crowd-pleaser, especially when you’ve had a couple of not-so-great GDP quarters before. So, all in all, it was all enough to take the Kiwi to the top spot and then some by the Friday close!

🟢 Bullish Headline Arguments

Dairy auction prices in New Zealand rose for the second successive auction. Both overall prices and key whole milk powder (WMP) prices jumped by 4.6% (vs. 2.7% previous)

New Zealand’s current account deficit shrank from 4.66B NZD to 4.21B NZD in Q2, marking its second consecutive quarterly decrease

New Zealand’s GDP grew by 0.9% in Q2, more than twice the 0.4% uptick expected and better than the -0.1% reading in Q1

🔴 Bearish Headline Arguments

BusinessNZ: New Zealand’s service sector weakened from 48.0 to 47.1 in August; “Negative comments received were strongly dominated by uncertainty regarding the upcoming General Election, as well as continued adverse economic conditions”

Westpac: New Zealand household confidence fell 2 points from 83.1 to 80.2 in September as living and mortgage costs continue to rise

New Zealand’s trade deficit widened from 1.2B NZD to 2.3B NZD in August as weaker Chinese demand weighed on exports

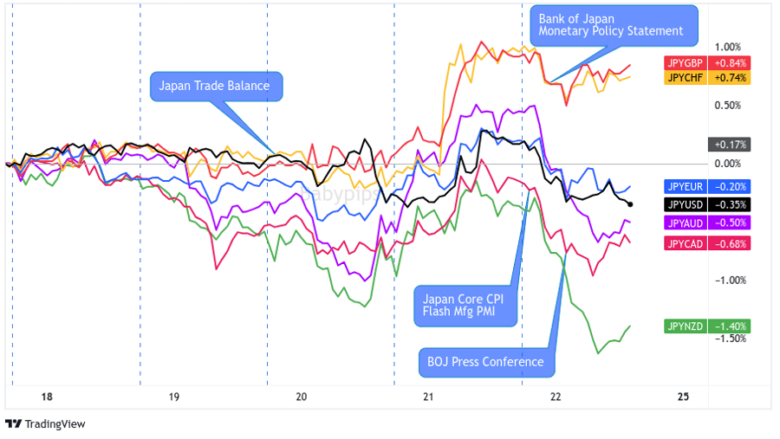

JPY Pairs

Overlay of JPY vs. Major Currencies Chart by TradingView

The Japanese Yen had a bit of a bumpy ride this week, and it mostly leaned on the negative side of things. One reason might be the positive vibes coming from Asia, especially with China giving its economy a boost.

Plus, it’s likely that traders were pretty sure that the Bank of Japan (BOJ) would keep their monetary policy super easy at the Friday decision, and that anticipation didn’t do the Yen any favors either.

Now, there was a moment when the Yen put on its superhero cape during a hawkish Fed event, creating a strong risk-off vibe that had traders running to safe havens.

But it seems that rally was short-lived, and the mood changed during the U.S. session on Thursday. That shift might have had something to do with the U.S. jobless claims numbers coming in better than expected, supporting the idea of a “soft landing.”

Then, when the BOJ finally made its statement on Friday, they did what everyone expected – kept those ultra-low interest rates unchanged at -0.10%. That pretty much sealed the deal for the Yen’s bearish move for the rest of the week.

🟢 Bullish Headline Arguments

Japan’s trade deficit trimmed from 0.60T JPY to 0.56T JPY in August as the decline in imports (-17.8% y/y) outpaced the decline in exports (-0.8% y/y)

Japan’s national core CPI grew by 3.1% y/y in August (vs. 3.0% expected, 3.1% previous)

🔴 Bearish Headline Arguments

BOJ kept ultra-low interest rates unchanged at -0.10% as expected; Gov. Ueda said that they’re “monitoring currency moves carefully” for their impact on inflation

Japan Flash Manufacturing PMI for September: 48.6 vs. 48.9 previous; Services PMI was 53.3 vs. 54.3; Employment in services sector declined while Mfg saw stronger growth; inflation grew at a slower pace; Outlook is positive but weakening

[ad_2]

لینک منبع : هوشمند نیوز

آموزش مجازی مدیریت عالی حرفه ای کسب و کار Post DBA آموزش مجازی مدیریت عالی حرفه ای کسب و کار Post DBA+ مدرک معتبر قابل ترجمه رسمی با مهر دادگستری و وزارت امور خارجه |  آموزش مجازی مدیریت عالی و حرفه ای کسب و کار DBA آموزش مجازی مدیریت عالی و حرفه ای کسب و کار DBA+ مدرک معتبر قابل ترجمه رسمی با مهر دادگستری و وزارت امور خارجه |  آموزش مجازی مدیریت کسب و کار MBA آموزش مجازی مدیریت کسب و کار MBA+ مدرک معتبر قابل ترجمه رسمی با مهر دادگستری و وزارت امور خارجه |

مدیریت حرفه ای کافی شاپ |  حقوقدان خبره |  سرآشپز حرفه ای |

آموزش مجازی تعمیرات موبایل آموزش مجازی تعمیرات موبایل |  آموزش مجازی ICDL مهارت های رایانه کار درجه یک و دو |  آموزش مجازی کارشناس معاملات املاک_ مشاور املاک آموزش مجازی کارشناس معاملات املاک_ مشاور املاک |

- نظرات ارسال شده توسط شما، پس از تایید توسط مدیران سایت منتشر خواهد شد.

- نظراتی که حاوی تهمت یا افترا باشد منتشر نخواهد شد.

- نظراتی که به غیر از زبان فارسی یا غیر مرتبط با خبر باشد منتشر نخواهد شد.

ارسال نظر شما

مجموع نظرات : 0 در انتظار بررسی : 0 انتشار یافته : 0